As the Affordable Care Act comes of age, a look behind the headlines

Know the facts behind the accusations and counter-claims so you can point your patients toward cost-effective coverage

The news media have focused on the federal online enrollment debacle. Easier enrollment options are available to people who live in federally run marketplace states, including direct enrollment. Strongly supported by America’s health insurance industry, direct enrollment lets potential enrollees purchase coverage directly from insurance companies participating in the marketplaces.

Problem 2: People lost their current coverage

This is a problem worth exploring—one that affects people who previously bought insurance on the individual insurance market. This is the market that offers people comparatively limited coverage, usually with no maternity care coverage, for comparatively high premiums.

So why are these individuals losing coverage?

They are losing coverage because, as of January 2014, new individual plans must abide by the 80/20 rule, abide by insurance protections, and cover 10 essential services with no cost sharing.

You may recall that, in August 2009, Americans were demanding that they be able to keep the health-care coverage they currently had, and President Barack Obama promised that they would be able to. Consequently, health insurance policies in effect before March 2010, when the ACA was signed into law, were exempted—“grandfathered”—from most ACA requirements. If people liked their old policies, they could keep them.

Grandfathered plans are exempt from:

the requirement to cover the 10 essential health benefits

the requirement that plans must provide preventive services with no patient cost sharing

state or federal review of insurance premium increases of 10% or more for non-group and small business plans

a rule allowing consumers to appeal denials of claims to a third-party reviewer.

Most ACA requirements apply to new policies—those offered after March 2010 and those that have been changed significantly by the insurance companies. Some examples of changes in coverage that would cause a plan to lose grandfathering include:

the elimination of benefits to diagnose or treat a particular condition

an increase in the up-front deductible patients must pay before coverage kicks in by more than the cumulative growth in medical inflation since March 2010 plus 15%

a reduction in the share of the premium that the employer pays by more than 5% since March 2010.

How many people are we talking about? Not the 40% of Americans who have employer-based coverage or the 20% of Americans on Medicare, Medicaid, or Tricare. This provision affects about 5% of the insured, as many as 15 million people—many with plans that offer little coverage for high premiums.

The ACA intention was that many people previously covered in the individual insurance market would find better and cheaper coverage in their state marketplaces. That may be a good option for people in states that have chosen to run their own marketplaces, and a good option for people in other states, too, as federal online enrollment issues get fixed.

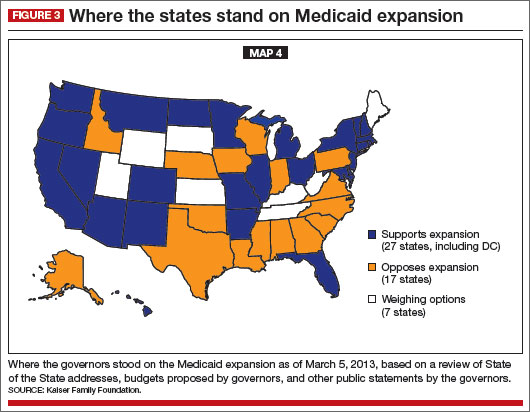

Problem 3: Medicaid expansion became a state option

When the US Supreme Court upheld the constitutionality of the ACA’s individual mandate, it also effectively turned the ACA Medicaid expansion into a state option.

Think of the Medicaid expansion as Medicaid Part 2. Regular Medicaid remains largely unchanged, with the same eligibility rules and coverage requirements.

The ACA included a provision under which every state would add a new part to its Medicaid program. Beginning in 2014, this part—the expansion—would cover individuals in each state with incomes under 138% of the federal poverty line—about $32,000 for a family of four in 2014. Medicaid expansion coverage is based only on income eligibility, a major change for women, many of whom currently qualify for Medicaid only if they’re pregnant.

Who would pay for the new coverage?

In 2014, 2015, and 2016, the federal government pays 100% of the cost of care for Medicaid expansion. From 2017 to 2020, the federal share gradually drops to 90%.

Medicaid expansion is an integral part of reducing the number of uninsured under the ACA and is expected to reduce the uninsured rate by almost 30% if adopted by every state. Medicaid expansion plus the ACA marketplaces were expected to cut our uninsured rate almost in half.

FIGURE 3 shows how states responded when the Supreme Court effectively converted the Medicaid expansion into an option, leaving us, again, with coverage gaps. Many of the states that have opted not to expand Medicaid are the same states that declined to operate their own state marketplaces, the same states with highest percentages of the uninsured.

The ACA has many interdependent parts. Make the Medicaid expansion a state option, and you end up with higher than expected rates of uninsured. Trigger big changes in the individual market when there are still bugs in the system, and people are left in the lurch.