Malpractice crisis: Causes of escalating insurance premiums, and implications for you

A shift in types of coverage is just one factor; but corrective options may be available to you.

What has led to the current malpractice crisis? There are 2 main theories.

Physicians, insurers, and hospitals generally blame lawyers and the litigation system for increasing the number of claims filed (claim frequency) and the average payout on claims (claims severity).

Attorneys and consumer groups argue that malpractice insurance goes through natural cycles in costs and charges. For the rise in premiums in the current crisis, they particularly blame decreased investment returns and poor pricing decisions by insurers.

Who’s right?

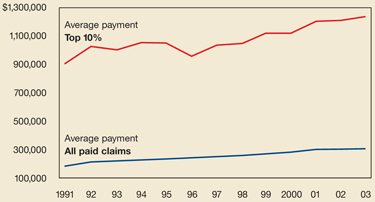

Research suggests that neither argument alone is persuasive. For instance, a study of the National Practitioner Data Bank, which collects results of all malpractice claims payments, found that claims severity did increase since 1991, but not during the current malpractice crisis period when adjusted for inflation: 52% from 1991 to 2003 but only 6% from 2000 to 2003.1 The highest growth rate has been in medium-sized awards, not the large ones you often read about. And, as always, claims severity growth varies among states (FIGURE 1).1

In contrast, when adjusted for population changes, Data Bank studies showed no significant nationwide increase in the number of paid claims from 1991 to 2003. Data from individual states also bear this out.1

Furthermore, studies of the relationship between claims’ payments and premiums have shown only a weakly positive relationship, suggesting other factors are involved. The argument that decreased investment returns have led to large price increases probably has some merit but does not explain the magnitude of the changes or the variation across states.

FIGURE 1

Amount of average paid claim, 1991-2003

So, what’s the answer for physicians?

Most likely, a combination of several changes has led to the recent crisis—increased claims’ costs, poor pricing decisions or cost projections by insurers, and decreased investment income. Rather than seeing these issues as distinct, it may be more useful to see their intrinsic relationships in leading to rapid premium increases and a malpractice crisis.

In this article, the first of 2, I discuss recent events influencing insurance premiums, which may also suggest to you avenues to explore in optimizing your own coverage. In part 2, I will address our current tort system and concrete proposals for change being pursued.

How premiums are determined

Almost all physicians carry professional liability (malpractice) insurance, either by choice or legal requirement. Coverage is usually purchased individually or by group from a commercial company or a physician-owned mutual company. Hospitals may purchase insurance or be self-insured, and their physician employees may be covered through those policies.

In theory, a tort system to resolve malpractice claims is supposed to serve as a negative incentive to physicians to practice high quality medicine. But the 1999 Institute of Medicine report on the occurrence and ramifications of medical errors, To Err is Human,2 provided evidence that the malpractice system has failed to accomplish this goal.

Unlike auto insurance, malpractice premiums are mainly determined by the class of physician (including type of work) and geography, rather than by an individual’s practice experience. Auto insurance premiums are adjusted according to the insured’s driving record. This is difficult to accomplish with malpractice insurance because claims experience is too variable over short periods of time.

Insurers take the following into account when they set premiums: 1) anticipated payouts to a class of physicians and the uncertainty of their estimate; 2) expected administrative expenses to manage the insurance; 3) future investment income; and 4) desired amount of profit. Information on past losses and expenses is used but, clearly, much of the determination involves complicated predictions.

Another characteristic that makes rate setting difficult is the length of time from the occurrence of an event to the filing of a claim to the resolution of that claim. On average, this is 4 to 5 years. The difficulty in predicting the liability for claims that have not yet been filed adds to the problem in setting premiums accurately.

How does your state manage rate setting?

Although malpractice has been a political issue at the federal level in the past few years, the reality is that, like most insurance, it is mainly regulated by the states.

States with substantial restrictions (17 states in 2004) require insurers to file rate changes and gain approval before prices can change.

States with less restrictive environments require such prior approval only if rate increases exceed a certain amount (23 in 2004) or only require notification after rates are changed (9 in 2004).1