Policy in Clinical Practice: Medicare Advantage and Observation Hospitalizations

© 2020 Society of Hospital Medicine

CLINICAL SCENARIO

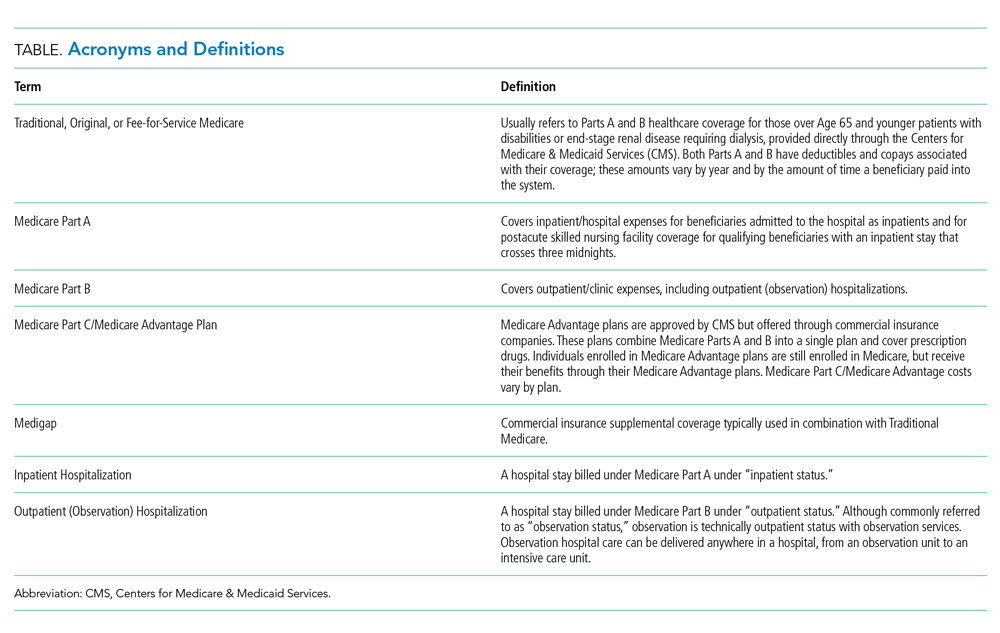

A 73-year-old man presents to the emergency department with sepsis secondary to community-acquired pneumonia. The patient requires supplemental oxygen and is started on intravenous antibiotics. His admitting physician expects he will need more than two nights of hospital care and suggests that inpatient status, rather than outpatient (observation) status, would be appropriate under Medicare’s “Two-Midnight Rule.” The physician also suspects the patient may need a brief stay in a skilled nursing facility (SNF) following the mentioned hospitalization and notes that the patient has a Medicare Advantage plan (Table) and wonders if the Two-Midnight Rule applies. Further, she questions whether Medicare’s “Three-Midnight Rule” for SNF benefits will factor in the patient’s discharge planning.

BACKGROUND AND HISTORY

Since the 1970s, the Centers for Medicare & Medicaid Services (CMS) has allowed enrollees to receive their Medicare benefits from privately managed health plans through the so-called Medicare Advantage programs. CMS contracts with commercial insurers who, in exchange for a set payment per Medicare enrollee, “accept full responsibility (ie, risk) for the costs of their enrollees’ care.”1 Over the past 20 years the percent of Medicare Advantage enrollees has nearly doubled nationwide, from 18% to 34%, and is projected to grow even further to 42% by 2028.2,3 The reasons beneficiaries choose to enroll in Medicare Advantage over Traditional Medicare have yet to be thoroughly studied; ease of enrollment and plan administration, as well as lower deductibles, copays, and out-of-pocket maximums for in-network services, are thought to be some of the driving factors.

The federal government has asserted two goals for the development of Medicare Advantage: beneficiary choice and economic efficiency.1 Medicare Advantage plans must be actuarially equal to Traditional Medicare but do not have to cover services in precisely the same way. Medicare Advantage plans may achieve cost savings through narrower networks, strict control of access to SNF services and acute care inpatient rehabilitation, and prior authorization requirements, the latter of which has received recent congressional attention.4,5 On the other hand, many Medicare Advantage plans offer dental, fitness, optical, and caregiver benefits that are not included under Traditional Medicare. Beneficiaries can theoretically compare the coverage and costs of Traditional Medicare to Medicare Advantage programs and make informed choices based on their individualized needs. The second stated goal for the Medicare Advantage option assumes that privately managed plans provide care at lower costs compared with CMS; this assumption has yet to be confirmed with solid data. Indeed, a recent analysis comparing the overall costs of Medicare Advantage to those of Traditional Medicare concluded that Medicare Advantage costs CMS more than Traditional Medicare,6 perhaps in part due to risk adjustment practices.7