Financial Fallout

Not once has Vanessa Yasmin Calderón regretted her decision to go into primary care, but she admits she’s disquieted by the amount of debt she’s accumulated while attending the University of California at Los Angeles for medical school and Harvard University’s Kennedy School of Government in pursuit of a master’s degree in public policy.

“I will be 30 years old when I graduate,” says Calderón, who plans to receive her medical degree in 2010. “Right now, I have no retirement account, and I’m staring at loads of debt in a bad economy. There’s a lot to think about.”

Calderón estimates she will have more than $146,000 in loans when she graduates—a daunting sum for someone who used scholarship money and a part-time job to put herself through college. Although Calderón is committed to a career in emergency or general internal medicine (IM), she has watched many of her peers forgo primary care in favor of anesthesiology, dermatology, and surgical specialties—partly because they are worried about how they are going to pay back their education debt.

“I guarantee you that primary care is being the most affected by rising debt,” says Calderón, vice president of finances for the American Medical Student Association (AMSA).

Her personal observations correlate with more than 15 years’ worth of published medical studies that have found compensation plays a role in dissuading medical students who are facing mountains of debt from choosing primary care. That includes careers in IM and, by extension, careers in HM, as more than 82% of hospitalists consider themselves IM specialists, according to SHM’s 2007-2008 “Bi-Annual Survey on the State of the Hospital Medicine Movement.” This doesn’t bode well for the nation’s future, experts say, because primary care and IM comprise the foundation of our nation’s healthcare system.

While the steep decline in IM recruits has leveled off in recent years, the number of medical students choosing IM residency (2,632 seniors entered three-year IM residency programs in 2009) is nowhere near the high point (3,884) of the mid-1980s, says Steven E. Weinberger, MD, FACP, senior vice president for medical education and publishing for the American College of Physicians (ACP).

“If there is not a change in how we support students going through medical school, how can we be surprised when they choose a higher-paying specialty?” says Michael Rosenthal, MD, professor and vice chairman of academic programs and research in the Department of Family and Community Medicine at Thomas Jefferson University in Philadelphia.

Loan Obligations

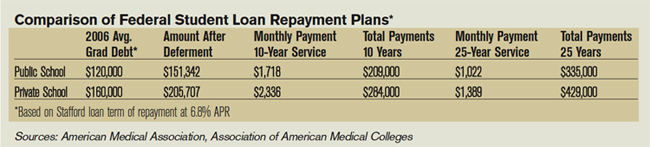

In 2006, more than 84% of medical school graduates had educational debt, with a median debt of $120,000 for graduates of public medical schools and $160,000 for graduates of private medical schools, according to a 2007 report by the Association of American Medical Colleges (AAMC). In comparison, the same report shows that, in 2001, the median debt for public and private medical school graduates was $86,000 and $120,000, respectively.